Should You Buy a House in India in 2026? Sales Fell, Prices Didn't — Here's Why

Home sales just hit a 4.5-year low — yet prices haven't budged. The gap between those two facts is the whole decision.

Short answer: Maybe — but for reasons most headlines get wrong. In Q1 2026 (Jan–Mar), home sales across India’s top nine cities fell about 13% year-on-year to 98,761 units — the first time a quarter slipped below 1 lakh sales in 18 quarters (~4.5 years), per PropEquity. The instinct is “demand fell, so prices must fall, so I’ll wait.” But prices didn’t fall — they rose ~2% (ANAROCK). The market didn’t get cheaper. It froze. And a frozen market is a very different thing to buy into than a falling one.

Sales fell. Prices didn’t. That’s the whole story.

Normally, when buyers vanish, prices follow them down. This time they split. Buyers stepped back, and prices stayed put — even ticked up. To understand whether to buy, you have to understand why those two things came apart, because the gap between them is exactly where you, the salaried buyer, are standing.

Why won’t prices drop if 6 lakh flats are empty?

By the end of Q1 2026, around 6 lakh ready flats were sitting unsold across the top cities. Builders even launched ~26% more new homes than a year earlier, while sales were falling. So why no discount?

Two reasons:

- Builders can wait. You can’t. Land, cement, steel and loan interest are all expensive. A developer will hold an empty flat for months before cutting the printed rate card. Time pressure is on the buyer, not the seller.

- The glut is in the wrong homes. Most of the unsold stock is premium — above ₹1 crore. Unsold inventory in the ₹2–5 crore band rose ~46%. Builders chased margin and overbuilt luxury, while the affordable ₹50–70 lakh home most salaried buyers actually want got scarcer.

So the market has “too many homes” and “too few homes you can afford” at the same time. That’s not a shortage — it’s a mismatch. And it squeezes you from both sides: prices firm, options thin.

What actually froze the buyers? Fear.

Open any business page: over 1 lakh tech jobs were cut in 2026, nearly 29,000 in May alone. Bengaluru, Hyderabad and Pune — the cities where software professionals buy homes — felt it first. The person who a year ago was ready for a ₹75 lakh home loan is now watching their own job and thinking, what if the appraisal doesn’t come? What if my name is on the list?

When people are scared, they freeze the biggest commitment first — and nothing is bigger than an EMI. One person pausing is caution. Lakhs pausing at once is a frozen market.

A market is never cheap when everyone’s buying, and never worthless when everyone’s afraid. The right home isn’t the lowest price — it’s the one you can pay for and still sleep at night.

So is it a crash? No.

Property analysts are clear: this is consolidation, not collapse. Demand hasn’t disappeared; decisions have just slowed. Both sides are real — the builder’s cost pressure is real, and the buyer’s job fear is real. The villain isn’t a person. It’s the cycle: fear spreads, everyone waits, and the waiting itself becomes a price.

What to do

- Don’t wait for a price crash that isn’t coming. List prices are firm. What has opened up is negotiating room on individual deals — discounts, free parking, GST adjustments. In a frozen market, the builder picks up the phone. This is the patient buyer’s first real opening in years.

- Separate “cheap” from “valuable.” A ₹1 crore flat that never fills isn’t cheap — it’s trapped money. A ₹70 lakh home your family lives in, with an EMI that fits your salary, is valuable even at a higher price.

- Decide on three numbers, not the news. How secure is your job? What share of your salary is the EMI? How many years will you live there? Those three own your decision. The builder’s “buy now” and the WhatsApp group’s “wait” are both noise.

Take action

Sources

- PropEquity — Q1 2026 residential sales, top 9 cities (via Construction World)

- ANAROCK — Q1 2026 housing report, top 7 cities (via Business Standard)

- Newsbytes — IT hiring freeze and housing demand, Q1 2026

- BizzBuzz — India tech-sector layoffs cross 1 lakh in 2026

- Outlook Money — Q1 2026 residential market, consolidation framing

Are house prices falling in India in 2026?

No. Despite home sales falling about 13% year-on-year in Q1 2026, average residential prices in the top cities actually rose around 2% quarter-on-quarter (ANAROCK). Sales fell, but prices held firm — the market froze rather than corrected.

Why are home sales falling if prices aren't?

Buyers — especially salaried IT professionals in Bengaluru, Hyderabad and Pune — turned cautious because of tech-sector layoffs (over 1 lakh tech jobs were cut in 2026) and Middle East / Iran-war uncertainty that made NRI investors pull back. Developers kept prices firm because land, material and financing costs stayed high and they can afford to hold unsold stock.

How many flats are unsold in India right now?

Around 6 lakh flats were unsold across the top cities by the end of Q1 2026 (ANAROCK). The glut is concentrated in homes above ₹1 crore — unsold stock in the ₹2–5 crore band rose about 46% — while affordable supply actually shrank.

Is this a property market crash?

No. Analysts call it a phase of consolidation, not a crash. End-user demand is stable in many markets; buyers are simply taking longer to decide. It is a frozen market, not a collapsing one.

Should I buy a house now or wait?

It depends on your own numbers, not the headlines: how secure your job is, what share of your salary the EMI takes, and how many years you'll live in the home. A frozen market gives patient buyers more room to negotiate on individual deals, even if list prices don't drop.

The India–UK Trade Deal Isn't About Cheaper Whisky

The headline is Scotch. The real money is in export jobs, a five-year salary waiver, and a 2027 carbon tax nobody's showing you.

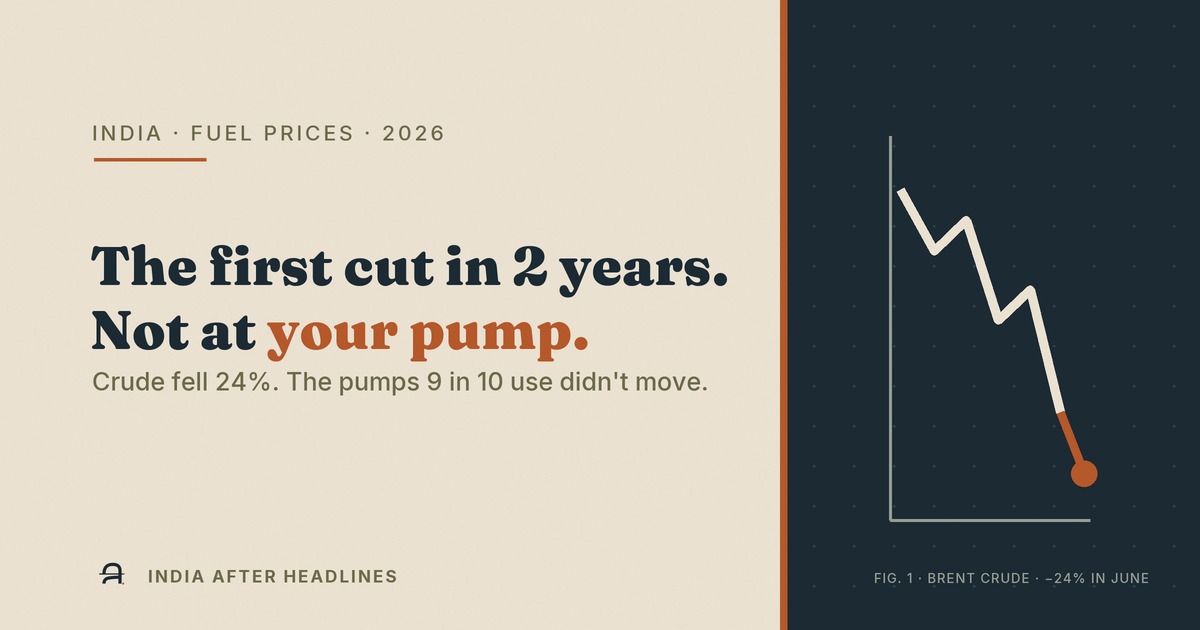

Petrol Just Got ₹5 Cheaper in India — for the First Time in 2 Years. So Why Is Your Pump Still Charging ₹102?

Crude crashed 24% in a month. One retailer cut prices. The pumps 9 out of 10 of us use didn't move a paisa. The gap between those two facts is the whole story.

From 1 July 2026, Your Credit-Card Reward Points Quietly Drop to Zero on the Spends You Use Most

A 'terms updated' email feels like a non-event. For the points you've been quietly banking on bills, UPI, insurance and school fees, it isn't.